Blog overview

Start using SimpledCard immediately?

Check out our packages or contact one of our experts directly!

Cross-border transactions are payments where the receiver and payer are in two different countries. These transactions are often more expensive than domestic payments. They simply involve more parties who pass on their costs. A change in European legislation, Cross-Border Privacy Rules 2 (CBPR2), makes it mandatory to transparently display prices in transactions in non-euro countries.

Organisations that trade internationally often do many cross-border transactions every day. It is a big part of their daily operations. It is therefore extremely important for these organisations to make such payments as secure, efficient and inexpensive as possible. This makes collaborations a lot easier.

Within Europe, of course, there is a lot of trade. And so there are many movements of money between different countries. Not all of these countries have the Euro as a means of payment. Think of Norway, Denmark or Hungary. Reason enough to establish clear regulations around cross-border payments and exchange fees.

The CBPR legislation provided more clarity back in 2009. The regulation meant leveled charges in cross-border transactions within Europe. The new amendment to this law, CBPR2, makes the cost of payment transactions within the European Union even more transparent.

❯ What are cross-border transactions?

❯ What is CBPR and what does CBPR regulate?

❯ Who oversees CBPR regulations?

❯ What has been changed by CBPR2?

❯ As SimpledCard, what do we do with cross-border transactions?

What are cross-border transactions?

Cross-border transactions, known internationally as cross-border payments, can be carried out in several ways. Bank transfers and credit card payments are the most common ways. Cross-border transactions are often subject to currency exchange fees. These are charges for changing from one currency to another.

- A credit card is a widely used and often the easiest way to make online payments to another country. All you then have to do is enter your card details. An example is when making an online purchase in a Swedish webshop in kronor. This often involves high transaction and exchange fees.

- Organisations also do a lot of online transfers. When the transfer is made to a business account with a currency other than euro, this is called cross-border. Given the large number of these transactions at organisations, the additional exchange costs and fluctuating exchange rates can then quickly add up.

- It is also possible to use a Dutch debit card to withdraw money from ATMs and ATMs outside the euro zone.

What is CBPR and what does CBPR2 regulate?

The first and original regulations (Regulation 924/2009) required that charges on cross-border transactions could not be higher than for an equivalent domestic payment in euro. This ensured lower charges on all cross-border transactions in the euro area. Note that charges are not the same as the exchange rate. The CBPR regulations do not specifically name which exchange rate should be used to calculate a transaction.

In the non-euro zone, cross-border transactions in euro are still expensive. The aim of the supplementary regulation to CBPR is to address this problem. The European regulation applies to all European Union member states.

Who oversees the CBPR2 regulations?

In the Netherlands, the Financial Markets Authority oversees the regulation of cross-border payments and foreign exchange fees, and so this case CBPR2.

What has been changed by CBPR2?

❯ From payments involving different currencies (from non-euro area member states), the charges become the same;

❯ There should be active information about any fees charged with each transaction.

The foreign exchange service provider is obliged to provide the following information.

At ATMs and ATMs:

❯ The cost of the transaction, expressed as a percentage of the most recent exchange rates;

❯ The payable amount of the transaction in the payer's currency;

❯ The payable amount of the transaction in the beneficiary's currency.

For online transfers to another payment account:

❯ The expected currency exchange cost of the transfer;

❯ The expected amount of the transfer in the payer's currency;

❯ The expected amount of the transfer in the beneficiary's currency.

Source: AFM

As SimpledCard, what do we do with cross-border transactions?

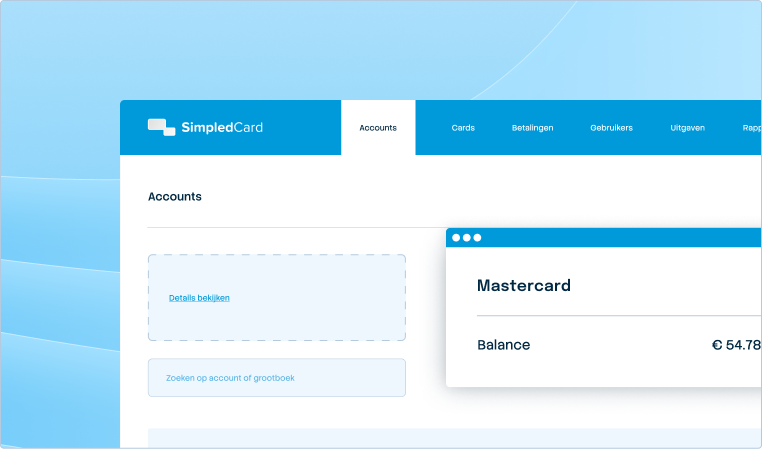

SimpledCard makes it easy and insightful to view the exchange rates of completed transactions. Every time a cross-border transaction takes place, the exchange rate is displayed in the system.

Transactions made with a SimpledCard payment card in a currency other than euro, the card's currency, are automatically converted to euro at the MasterCard conversion rate. The conversion rates are shown on the Mastercard website. Unlike many other banks and payment solution providers, SimpledCard does not add any fees itself.

If conversion of a transaction is chosen at the ATM or payment terminal itself, the conversion will be carried out by another party. A different exchange rate will then apply and additional fees may be charged by this party. They are then obliged to disclose this at the time of the transaction. The exchange rates of these transactions are not reflected in the SimpledCard system.

So for SimpledCard users, nothing actually changes with the CBPR2 law change. SimpledCard transactions remain favourable and, from now on, this is even more insightful through exchange rate reporting. Within the SimpledCard system, you can at any time print out a report of all cross-border transactions with corresponding conversion ratios.

If you want to know more about the CBPR2 regulation or our transparency for cross-border transactions? Then get in touch with our team of experts.

News around legislation and CBPR2